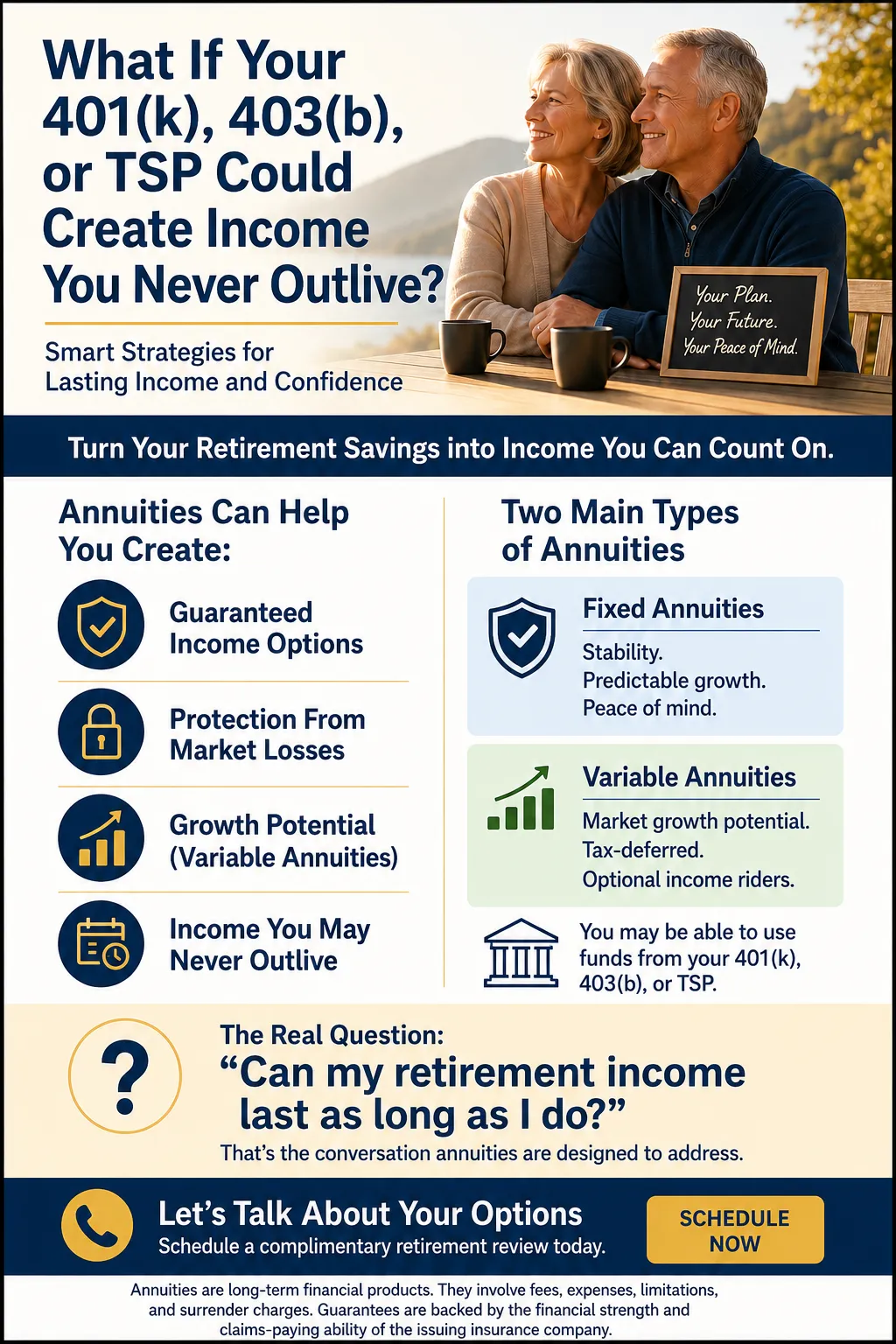

What If Your 401(k), 403(b), or TSP Could Create Income You Never Outlive?

WHAT IF YOUR 401(k), 403(b), OR TSP COULD CREATE INCOME YOU NEVER OUTLIVE?

Smart Retirement Strategies for Lasting Income and Greater Confidence

For many Americans, retirement planning revolves around building the biggest account balance possible.

We’re taught to contribute to our 401(k), 403(b), or TSP, invest consistently, and hope the market grows enough to carry us through retirement.

But there’s one major question many people don’t ask until it’s almost too late:

How Do You Turn That Retirement Balance Into Reliable Income for Life?

That’s where annuities often enter the conversation.

THE RETIREMENT SHIFT MOST PEOPLE MISS

During your working years, retirement accounts are focused on growth.

But retirement itself is no longer only about growth. It becomes about:

✔ Creating predictable income

✔ Protecting savings from major market losses

✔ Managing longevity risk

✔ Reducing fear of running out of money

The challenge is that traditional retirement accounts like a 401(k), 403(b), or TSP were designed primarily as accumulation vehicles.

They do not automatically guarantee lifetime income.

That’s why many retirees and pre-retirees explore options like fixed annuities and variable annuities.

WHAT IS AN ANNUITY?

An annuity is a financial product offered by insurance companies that can help convert retirement savings into a stream of income.

Depending on the type of annuity, it may offer:

✔ Guaranteed income

✔ Principal protection

✔ Tax-deferred growth

✔ Market participation

✔ Optional lifetime income riders

Not every annuity is the same, and understanding the differences matters.

FIXED ANNUITIES: STABILITY AND PREDICTABILITY

A fixed annuity is designed for people who want more stability and less exposure to stock market volatility.

Potential Benefits of a Fixed Annuity

✔ Guaranteed interest rates

✔ Protection from market downturns

✔ Predictable future income options

✔ Tax-deferred growth

✔ Less emotional stress during market swings

For someone nearing retirement, a fixed annuity may help create a more conservative portion of their retirement strategy.

Who Might Consider a Fixed Annuity?

A fixed annuity could be a fit for someone who:

✔ Is concerned about stock market losses

✔ Wants more predictable retirement income

✔ Values safety over aggressive growth

✔ Wants to protect a portion of retirement savings

Many retirees use fixed annuities to help cover essential expenses such as:

• Housing

• Utilities

• Food

• Insurance premiums

The goal is often to create a “retirement paycheck” that continues even after leaving the workforce.

VARIABLE ANNUITIES: GROWTH POTENTIAL WITH INCOME FEATURES

A variable annuity works differently.

Instead of earning a fixed interest rate, your money is invested into market-based subaccounts similar to mutual funds.

This means your account value can rise or fall based on market performance.

Potential Benefits of a Variable Annuity

✔ Opportunity for market growth

✔ Tax-deferred investing

✔ Optional guaranteed income riders

✔ Lifetime income options

✔ Ability to participate in market upside

Some people like variable annuities because they want continued market exposure while also adding income guarantees through optional riders.

Things to Consider

Variable annuities can include:

• Higher fees

• Market risk

• More complexity

• Surrender periods

Because of this, they’re often best evaluated carefully with a licensed financial professional.

COULD AN ANNUITY WORK WITH YOUR 401(k), 403(b), OR TSP?

Many people don’t realize they may be able to:

✔ Roll over old retirement accounts

✔ Transfer qualified retirement funds

✔ Reposition part of their retirement savings

✔ Create future income strategies

This does not mean moving all your retirement money into an annuity.

In many cases, people simply explore whether allocating a portion of their savings toward guaranteed income could improve retirement confidence.

A Balanced Retirement Strategy May Include:

• Market investments

• Cash reserves

• Social Security

• Pension income

• Fixed annuities

• Variable annuities

The right mix depends on your goals, risk tolerance, time horizon, and income needs.

THE REAL QUESTION ISN’T JUST GROWTH

Many retirees eventually realize the most important question isn’t:

“How Large Is My Retirement Account?”

It becomes:

“CAN MY RETIREMENT INCOME LAST AS LONG AS I DO?”

That’s the conversation annuities are designed to address.

FINAL THOUGHTS

A fixed annuity or variable annuity may not be right for everyone, but for some people, they can help create:

✔ Greater retirement confidence

✔ More predictable income

✔ Reduced market anxiety

✔ Long-term income planning

If you’re approaching retirement or reviewing old 401(k), 403(b), or TSP accounts, it may be worth exploring how guaranteed income strategies fit into your overall financial picture.

The right strategy isn’t always about chasing the highest returns.

Sometimes it’s about creating income you may never outlive.

CALL TO ACTION

Ready to Explore Your Retirement Income Options?

Schedule a complimentary retirement review to learn how guaranteed income strategies may fit into your overall financial plan.